In May, U.S. inflation levels were well above forecasts. We have witnessed two months in a row of inflationary levels not seen in decades. The Federal Reserve has argued that this inflation is temporary or "transitory." But we should investigate further. We do not want any surprises. In May, the 12-month core inflation rate (excluding energy and food prices) increased from +3.0% in April to +3.8%.

| | | | | | How to Address Inflation Right Now |

|

| Dear Reader,

In May, U.S. inflation levels were well above forecasts. We have witnessed two months in a row of inflationary levels not seen in decades. The Federal Reserve has argued that this inflation is temporary or "transitory."

But we should investigate further. We do not want any surprises.

In May, the 12-month core inflation rate (excluding energy and food prices) increased from +3.0% in April to +3.8%.

This was the sharpest increase in 29 years.

The consensus of economists had forecast a core inflation rate of +3.4% for May.

If you think that was high, check out this figure.

The inflation rate (including energy and food prices) climbed to +5.0% in May 2020 from +4.2% in April 2021. Here, too, the number beat economists' expectations of +4.7%.

Only one of these experts had correctly estimated the May increase in the inflation rate. His prediction was also the highest of all.

How can it be that economic experts permanently lag so behind reality?

Is their assessment perhaps influenced by the attitude of the central banks, which stubbornly chant the mantra of only a temporary increase?

The Fed said this week that it would likely raise interest rates two times by 2023. But that doesn't seem to reflect the reality that higher prices are caused by rising demand and other challenges in the supply chain.

Once again, as a reminder: until August 2020, the Fed's inflation target was +2.0%: In the event of a sustained overshoot, the central bankers then wanted to intervene.

But ten months ago, Fed Chairman Jerome Powell said the Fed wanted to "tolerate moderate inflation above +2.0%."

As is well known, the (lower) core inflation rate is the decisive factor for the Fed:

|

|

| | |

As you can see, there has been no situation in the past ten years in which monetary policy would have had to be changed due to the trend in monetary devaluation.

But with a core inflation rate of +3.8%, can the Fed, in all seriousness, still speak of a "tolerable" overshoot? Hardly. Unless that is, we have indeed just seen the peak of monetary devaluation.

One reason for this assumption is probably the following chart:

|

|

| | |

Again, you can see the core inflation rate, but this time only for the past 24 months. What is significant here is the dip in the months April to June 2020.

For these months, the low starting point on which the last comparative rates were calculated applies. From July onward, the core inflation rate will again be calculated from a somewhat higher level.

Global supply chains: Soon back in sync?

The most important reason for monetary depreciation is the asynchronization of the global supply chains due to the lock-down measures.

Containers arriving at destination ports were not emptied for weeks, reducing the availability of cargo space. Plenty of sand got into this fine-tuned wheelwork of global supply chains, which for many years had ensured "just-in-time" production (when raw products were delivered).

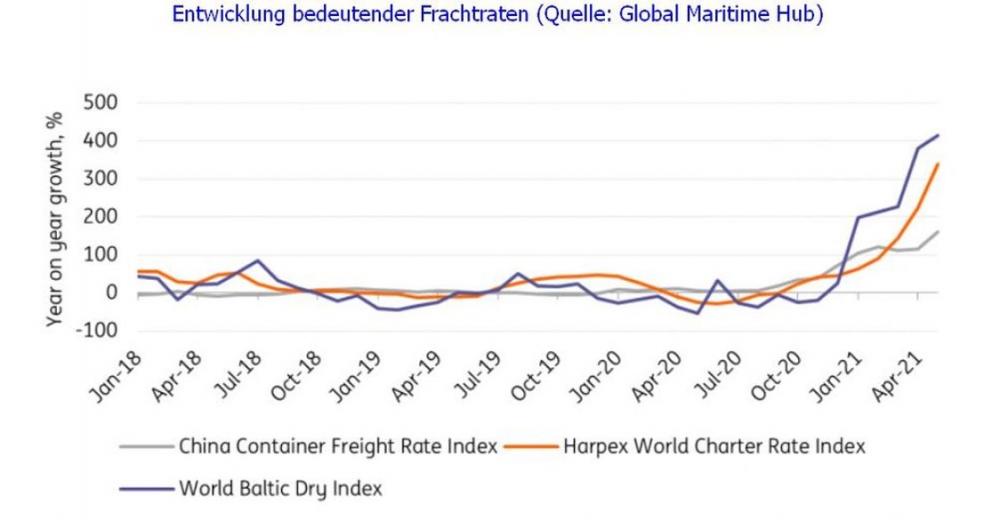

We are now seeing a fierce battle for container capacity between manufacturers and suppliers worldwide. This has caused the transport rates for freight space to explode. The chart below reflects an explosion in freight rates over the last year.

|

|

| | |

It is possible that the Fed - and with it other central banks - has so far expected a swift re-synchronization of these gears.

But recent news from southern China from the important ports of Yantian and Shekou near Shenzhen and Nansha in the metropolis of Guangzhou make us sit up and take notice.

According to the world's leading online platform for leasing and trading of shipping containers, Container xChange, the aforementioned ports recorded a decline in container availability of between -16.4% and -29.6% in the last five weeks due to Covid-19 closures (source: Global Maritime Hub)!

Freight rates will therefore remain high and probably even continue to rise.

This is due to the disorganized supply chains, lack of freight alternatives, picking up demand due to the economic revival, congestion, and temporary port closures, causing further delays and thus further reducing transport capacity.

The price pressure will be passed on to consumers as best that companies can.

Therefore, a side effect of persistent inflation is the pressure on margins, which in turn affects the development of corporate profits.

Even a stock market cannot ignore this in the long term.

We'll discuss this more in the days ahead.

Enjoy your weekend, |

|

| | | | | | |

|

|

No comments:

Post a Comment